企业新闻

News

-

APREA Witnesses the Official Listing of China's First Batch of Commercial Real Estate REITs on the SSE Today!

2026-06-18

June 18, 2026 — The first batch of four domestic commercial real estate public REITs was officially listed and began trading on the Shanghai Stock Exchange (SSE). The successful listing of these products marks a major milestone: after five years of intensive development, China's public REITs market has officially moved beyond a single infrastructure track. It has now entered a new, dual-driven development phase of "Infrastructure + Commercial Real Estate," marking a landmark event in the domestic real estate finance sector.

The listing ceremony boasted an unprecedentedly high-profile lineup of guests. Key leaders from the Shanghai Stock Exchange, heads of the four original asset owners corresponding to the REIT products, representatives from various fund management institutions, and project-specific securities firms were all in attendance. In addition, prominent representatives from leading industry asset management institutions and real estate operations companies gathered at the venue to participate in the entire core process, including speeches, signings, gift exchanges, and the striking of the opening gong.

David Chen (Chen Xiaoou), Chairman of APREA (Asia Pacific Real Estate Association) China and Chairman of F.O.G Assets, was invited by the SSE to attend the listing ceremony, witnessing this milestone moment of market expansion and upgrade for public REITs!

The four commercial real estate REIT products debuting on the SSE are:

-

China Universal Shanghai Real Estate Commercial REIT (508600)

-

CSC Shou農 Commercial REIT (508601)

-

Cathay Haitong Sasseur Commercial REIT (508602)

-

CICC Vipshop Commercial REIT (508603)

Together, the four products raised a total subscription scale of 20.333 billion RMB. Market enthusiasm reached unprecedented heights, with total subscription funds from offline and public tranches exceeding 500 billion RMB, fully demonstrating the high level of recognition that institutional and retail investors have for the commercial real estate public REIT category.

Core Overview of the Four Listed Products

1. China Universal Shanghai Real Estate Commercial REIT (508600)

-

Underlying Assets: Located in the Huangpu District of Shanghai, encompassing two Grade-A office buildings—Dingbao Mansion and Dingbo Mansion—along with supporting ground-floor retail spaces.

-

Pricing & Scale: Issued at 4.092 RMB per unit, with 1 billion units issued, totaling a scale of approximately 4.1 billion RMB.

-

Duration: The duration is 41 years, making it the longest-lasting vehicle among the four products.

-

Financials: Institutions forecast the distributable amount for the year 2026 to be 183 million RMB, corresponding to a distribution yield of 4.47%.

-

Ownership: The original asset owner, Shanghai World Expo Development Group, retains a 34% stake.

2. CSC Shou農 Commercial REIT (508601)

-

Underlying Assets: Longde Plaza, a mature, well-established shopping center in Changping, Beijing, which has been operational since 2008.

-

Pricing & Scale: Issued at 3.013 RMB per unit, with a total scale of approximately 3 billion RMB.

-

Financials: The forecasted distributable amount for 2026 is 170 million RMB, yielding a distribution rate of 5.64%, which ranks first among the four products.

-

Duration: Due to land-use right limitations, the product's duration is only 20 years.

-

Ownership: The original asset owners, Beijing Grain Group and Xijiao Farm, collectively hold a 34% stake.

3. Cathay Haitong Sasseur Commercial REIT (508602)

-

Underlying Assets: Xi'an Sasseur Outlets, opened in 2017, which serves as a leading regional outlet project.

-

Pricing & Scale: Issued at 5.531 RMB per unit, with a total scale of approximately 5.5 billion RMB.

-

Financials: The estimated distributable amount for 2026 is 275 million RMB, with a distribution yield of 4.97%.

-

Duration & Demand: The duration is 30 years. This product garnered the highest market enthusiasm, with an offline subscription oversubscription rate exceeding 100 times.

-

Ownership: The original asset owner, Sasseur (Xi'an) Shopping Plaza, retains a 41% stake.

4. CICC Vipshop Commercial REIT (508603)

-

Underlying Assets: The largest asset by volume among the four products, its underlying portfolio covers two Shanshan Outlets located in Zhengzhou and Harbin.

-

Pricing & Scale: Issued at 3.848 RMB per unit, with 2 billion units issued, totaling a scale of approximately 7.7 billion RMB.

-

Financials: The forecasted distributable amount for 2026 is 339 million RMB, with a distribution yield of 4.40%.

-

Duration & Demand: The duration is 31 years, with an offline subscription oversubscription rate of 68 times.

-

Ownership: The original asset owner, Shanshan Commercial Group, retains a 49% stake, representing the highest retention ratio among the original owners of the four products.

The Profound Significance of Commercial Real Estate REITs for the Industry

The smooth listing of these commercial real estate public REITs represents a core outcome of the pilot policies rolled out by the China Securities Regulatory Commission (CSRC) at the end of 2025.

From the Capital Market Perspective: This asset class bridges a vital gap in the public REITs asset category. It offers investors across the market a new option for stable, large-scale asset allocation, effectively diversifying investment channels.

From the Real Estate Industry Perspective: These products can effectively revitalize China's trillion-RMB pool of existing commercial property assets, unlocking securitization pathways for legacy commercial real estate. This shifts the industry's development logic away from traditional "heavy-asset development" toward refined "asset operations and management." Ultimately, it will drive a high-quality transformation of the commercial real estate sector, carrying immense strategic value for the long-term, healthy development of real estate.

more +

-

-

David Chen: Reshaping the New Landscape of Real Estate Investment in 2025 | 2025 Boao Real Estate Investment Conference

2026-06-18

The following is the keynote address delivered by David Chen at the 2025 Boao Real Estate Investment Conference.

David Chen (Chairman, F.O.G Capital & Asset Management Group; Independent Director, Yuexiu REIT): Thank you to the moderator, and thank you to Guandian. Before the session began, I watched a video tracing Guandian's journey from 2001 to 2025 — 25 years — with the faces of leading figures from the industry's most prominent companies flashing across the screen.

I was invited here today by Guandian and President Shitao to share a few thoughts. The topic I've been given is a broad one — themes of reshaping, investment, and the shifting landscape — so it won't be easy to cover comprehensively, but I'll offer an overview.

F.O.G in F.O.G Capital stands for Fields of Gold. Our core businesses are real estate investment and asset management.

I'd like to start with the broader context of our times. Looking across that 25-year span, the faces in the room today are quite different from those who sat here 25 years ago. Every era produces its own talent.

2020 was a pivotal year for the real estate industry. That was when the wave of developer debt defaults began — against the backdrop of the COVID-19 outbreak in China and the severe spread of the pandemic across the United States and Southeast Asia. The industry underwent profound disruption from that point, with the total scale of developer debt defaults eventually reaching RMB 15.8 trillion.

In the midst of this economic upheaval, China launched a landmark real estate financial product in 2021: publicly listed REITs. Those outside the industry may not fully appreciate the significance of this. Many people still don't know what a REIT is. Simply put, a REIT takes real estate assets with sound operations and stable cash flows and securitizes them — issuing shares that allow investors to access the steady income and capital appreciation of high-quality properties.

Fast-forward to 2024: the People's Republic of China celebrated its 75th anniversary, while across the Pacific, a familiar face returned to power in the United States — Trump 2.0 had begun. Set against this backdrop were the ongoing Russia-Ukraine conflict, turmoil across the Middle East, and a host of other major international developments.

Now, in 2025, let's take stock of where things stand — at home and abroad. Keeping our lens focused on real estate, since this is a real estate forum: where do the structural challenges lie? Let me run through a few:

First, developers have found themselves in an unprecedented crisis — debt default. In Hong Kong, many property companies had borrowed heavily in US dollars, as dollar-denominated debt was relatively accessible. But dollar debt carries high interest rates, and debt, like a mortgage, demands repayment. The defaults swept through the majority of China's major developers.

Second, the post-pandemic economic trajectory. The pandemic ended less than three years ago, and many people no longer want to discuss it. But the economic conditions we're navigating today have been profoundly shaped by what happened, and we cannot sidestep that reality.

Third, a collapse in consumer confidence. This morning over breakfast, I was speaking with a few program directors from Hainan Television about the changes in consumption on the island. Consumer confidence in Hainan is nowhere near where it was before the pandemic.

Fourth, global geopolitical instability. Returning to Trump 2.0: whatever one makes of him personally, his impact on China and the world at large is enormous. We need to take him seriously.

Against this backdrop, let's look at where major real estate enterprises now stand:

On the scale of developer defaults: between 2020 and 2025, 32 property companies accumulated liabilities of RMB 15.8 trillion — equivalent to 12.3% of 2024 GDP. Even as GDP growth was recovering last year, this debt overhang represented an extraordinary share of the economy. The companies involved need not be named; the scale of the defaults speaks for itself.

By 2024, maturing debt for the top 50 developers exceeded RMB 800 billion — approaching one trillion yuan. And sales? Down 40% to 70% year-on-year depending on the city tier. This isn't a haircut; it's a collapse. A developer that used to sell 100 units can now sell only 30.

The risk contagion has been severe: project stoppages and construction halts across the country; an estimated 3 million housing units with delayed delivery; and RMB 3.7 trillion in real estate-related non-performing assets, based on banking sector data.

Policy responses have included state-owned enterprises taking over 70% of newly commenced projects, a "whitelist" mechanism to restructure and requalify property developers, and RMB 4 trillion in bank credit support. This morning's news also mentioned that the government has recently issued ultra-long-term, low-interest sovereign bonds to support large-scale infrastructure construction.

So what are the bright spots in an otherwise bleak landscape? Is there any light to be found?

On August 3, 2024 — three years after publicly listed REITs officially launched in 2021 — the National Development and Reform Commission (NDRC) issued a formal notice: going forward, REITs will be issued on a normalized, ongoing basis in China's financial markets.

This is significant. Normalized issuance means that after three years, this newborn asset class has been recognized — not just as a regulatory compliance exercise, but as a legitimate and enduring part of China's capital markets. The notice also removed earlier requirements for minimum yield thresholds, leaving pricing to market forces. In effect, REITs have learned to walk on their own.

Where does the REITs market stand today? We started with 9 REITs listed in 2021. We now have 73, with the most recent additions being two data center REITs. Total market capitalization exceeds RMB 200 billion. Asset types eligible for REITs issuance now span 10 to 11 categories.

Against this backdrop, let's also look at another set of numbers closely tied to the market: interest rates. The three-year savings bond rate stands at just 1.63%. The five-year-plus LPR — the benchmark for mortgage lending — is only 3.5%. Rates have fallen sharply across the board.

And this month, on August 1st, the People's Bank of China released its priorities for the second half of the year: continued easing, continued rate cuts. The one-year rate is expected to fall below 0.7%; three-year lending rates are expected to drop below 1%.

This signals that the government is actively stimulating consumption and discouraging savings. When deposits offer no returns, behavior changes — we've seen this play out in Japan. This environment is fundamentally different from anything we saw before the pandemic. The past five years have brought extraordinary change.

At the same time, new signals are emerging. At the Lujiazui Forum on June 18, 2025, one development stood out among the many financial announcements: the QFLP (Qualified Foreign Limited Partnership) program — opening China's market to qualified overseas investors. This has already prompted a number of foreign funds to begin structuring domestic real estate private equity funds in renminbi.

The expansion in scope is substantial. Funds can now invest in domestic private equity funds through a fund-of-funds structure; pilot funds can participate in non-public issuances of A-shares, and even in non-performing asset disposal — a significant signal. Investment instruments have expanded from equity to bonds, and may now include public REITs and STAR Market investments. The pilot program's ceiling has doubled from USD 100 billion to USD 200 billion, and I expect that figure will continue to grow. Shanghai has set its sights on becoming Asia's largest QFLP center — surpassing Singapore. That is a meaningful ambition.

There is also something else worth watching — a new frontier at the intersection of finance and real estate: RWA, or Real World Assets. RWA means putting real-world assets on the blockchain. Property titles no longer need to be on paper; every transaction, from the moment an asset is created through every subsequent transfer, is permanently recorded on-chain and fully traceable. Transactions are executed in digital currency. Hong Kong has already passed legislation on RWA, and many firms are actively planning product issuances.

In time, REITs won't need to be traded on public stock markets at all. Smaller assets will be able to raise capital online via RWA. With blockchain providing the evidentiary foundation, the legal, compliance, and informational overhead is dramatically reduced. And the bigger picture here is asset digitization — a concept that has already become a major force in the United States.

At last night's dinner during this forum, several experts raised the topic of the tariff war. I would argue that tariffs, while important, are not the most critical issue — that's a government-level trade negotiation. What deserves equal attention is the transformation being driven by asset digitization. In the United States, stablecoins are now being linked to U.S. Treasuries, suggesting that the dollar may eventually evolve into a form of digital currency. If so, the dollar's global dominance may be reasserted in an entirely new form, once again leading the world's monetary and financial markets. These are trends worth watching carefully — including the financialization of real estate through REITs, which I believe this forum should be actively advocating for.

In closing, I want to return to the author Wang Xiaobo, whose prescient vision continues to resonate. He wrote of the Golden Age, the Silver Age, and the Iron Age. Are we now in an Iron Age? On the surface — based on everything I've laid out — it certainly looks that way. But beneath the iron, what lies buried?

I was honored to be invited by Guandian to speak on this sweeping topic in 2025 — a year that marks both the 25th anniversary of this forum and a moment of profound reckoning for the industry. What should we expect?

Real estate policy frameworks are being restructured. With debt loads so elevated, government intervention has become necessary. The approach has shifted from blanket restrictions to targeted, precision support — for example, lifting purchase restrictions in Beijing's outer ring. The question is whether these measures will cut to the heart of the issue and restore consumer confidence in housing.

The competitive landscape for developers has also been permanently altered. The top 10 developers now account for 35% of the market. Private developers have seen sales fall by roughly 30% year-on-year — a severe blow. The industry is moving away from pure development toward diversification and services: long-term rental housing, property management, commercial management, contract development. Contract development — building for others rather than investing your own capital — is actually the mainstream model in the United States. A typical American home is built by two parties: an investor and a developer, where the developer is essentially a contractor. China's contract development model is still version 1.0, a pure asset-light service play without capital co-investment. In the U.S., developers typically co-invest 1% to 5%, and many large institutions maintain a small-equity-stake operating model.

The industry's operating logic is shifting from "develop and sell" to a full cycle of "invest, finance, build, manage, and exit."

As I observe the current environment, I'll say this about distressed asset acquisition: it's a bit early. The window is beginning to open, but the timing isn't quite right yet.

What I do see clearly is that the activation of the REITs market is likely to be one of the most important trajectories for real estate's transformation.

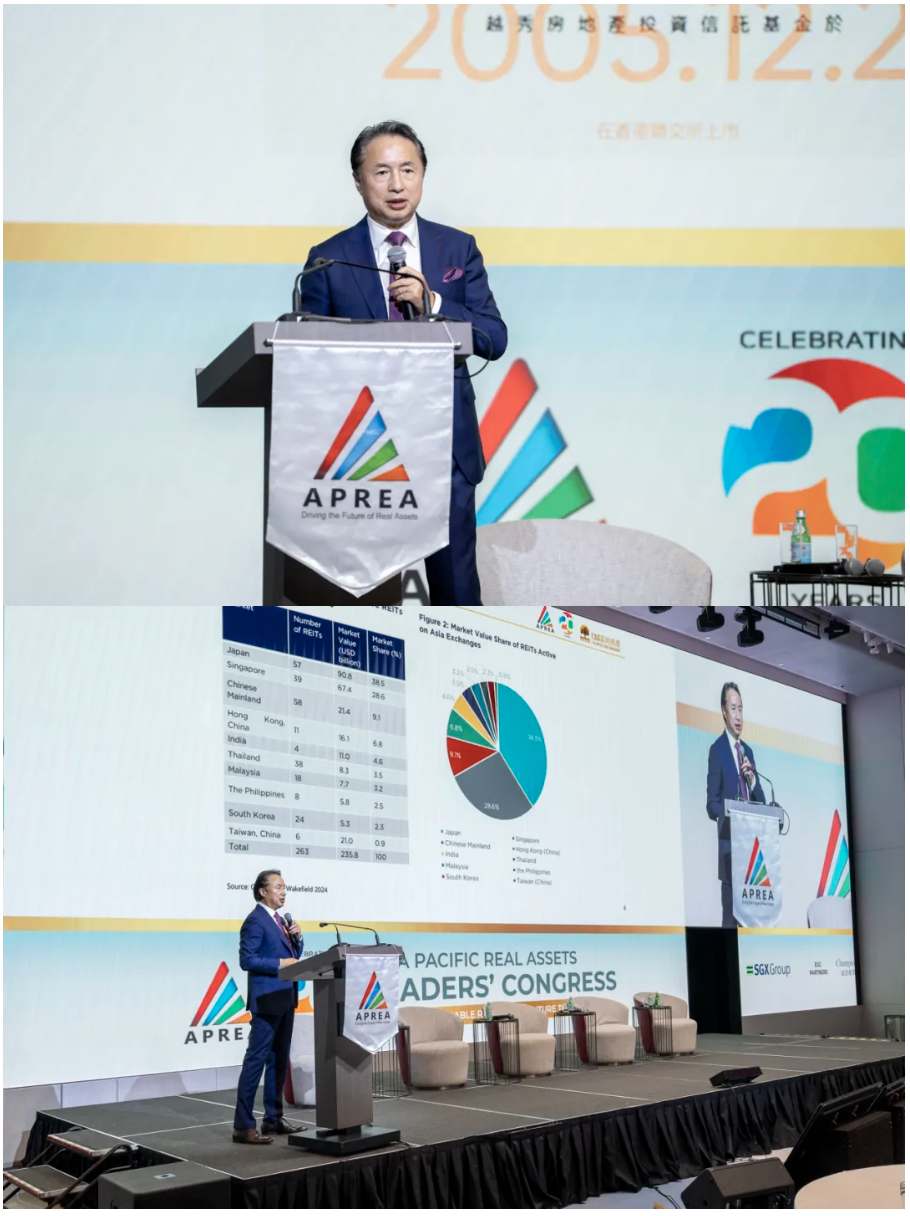

China's REITs market currently stands at over RMB 200 billion — roughly USD 30 billion. Zoom out to the global picture: Asia as a whole is USD 240 billion, the United States is USD 1.67 trillion, and the total global REITs market exceeds USD 2.6 trillion. China's share remains small.

The global REITs market has become a mature financial category, spanning 42 countries and territories and serving a population of 5 billion people. Even Vietnam and Kenya now have REITs.

The United States, as the originator, enacted REIT legislation in 1960. Three of the earliest U.S.-listed REITs: Winthrop (delisted in 2014); and Pennsylvania REIT and Washington REIT — retail and diversified, respectively — both still active, with Washington REIT delivering annualized returns of 9.8%. By 1967, there were 10 U.S. REITs with a combined market cap of USD 200 million. By 1968, once the market grasped their value, that figure had jumped to USD 1 billion. Today, the U.S. market stands at USD 1.67 trillion — a roughly 1,670-fold increase over approximately 50 years.

The story of U.S. REITs is one of "born in a downturn, matured through globalization." That arc may well be replicated in China.

From 1960 to 2024, U.S. REITs delivered annualized total returns of 9% to 11%. Compare that to today's wealth management products, where finding a 4% return is considered a success. Those 9% to 11% returns come from two sources: annual REIT distributions, and share price appreciation driven by inflation and real estate value growth.

Among the top 10 U.S. REITs by market cap, the leading categories are not traditional real estate — they are logistics and communications infrastructure. And one sector has surged unexpectedly: data centers. During the three pandemic years, when I spoke with many U.S. REIT managers, data centers dominated investor interest. While the pandemic period was the worst three-year stretch for U.S. REITs overall, data centers were compounding at 30% annually.

Comparing Asian REITs to their U.S. counterparts: Asia's market only launched in 2000 — 40 years after the United States. Japan went first, followed by Singapore. In 2005, China's first REIT, Yuexiu REIT, listed in Hong Kong — a historic milestone. That same year, the Asia Pacific Real Estate Association (APREA) was founded, a major professional body dedicated to aggregating resources across the value chain and covering 18 countries globally.

Asia's total REITs market cap now stands at approximately USD 236 billion. Japan's market — at over USD 100 billion — is the largest in Asia. Japan offers a diverse range of asset types and distribution yields, and is worth studying closely. Singapore's REITs market is the most active in Asia and is truly global in scope, issuing REITs backed not just by Singapore assets but even U.S. assets. Distribution yields tend to run 6% to 7%, and sometimes up to 8% — a meaningful figure. Many Singapore-listed REITs hold assets in mainland China, which is directly relevant to us.

Hong Kong has 11 REITs with a combined market cap of approximately USD 25 billion, led by Link REIT and Yuexiu REIT. More than half of Hong Kong's listed REITs hold Chinese assets, making this market well worth our attention.

Yuexiu REIT listed in Hong Kong in 2005 as the world's first China-backed REIT — a development whose influence on today's REITs market is hard to overstate. Where has it gone since? It has built a powerful flywheel with Yuexiu Property Group, linking development, operations, and finance in a closed loop that most Chinese real estate companies lack — no REITs exit channel, no financing cycle.

Yuexiu REIT's journey unfolded in three phases. The 2005 IPO established an early blueprint for real estate securitization. In 2012, it made a landmark acquisition of Guangzhou IFC — valued at approximately HKD 15.4 billion, the largest real estate acquisition in Asia at the time. Since then, it has pursued a strategy of dynamic balance: concurrent expansion through acquisitions and strategic asset disposals, continuously growing and refreshing its portfolio. It has also been a financial innovator — issuing a rental housing quasi-REIT in 2018, one of the earliest long-term rental apartment securitizations in China. Yuexiu also has a presence in mainland China's public REITs market through Yuexiu Transport Infrastructure REIT. And last November, we led the issuance of the country's first privately placed commercial real estate ABS backed by held-for-investment property — a milestone worth remembering.

The history of real estate securitization in China, from 2021 to today, shows REITs steadily emerging as an unexpected force at the intersection of real estate and finance. The ecosystem has matured through several turning points, from early exploration to normalized public issuance. The C-REITs family now encompasses quasi-REITs, ABS, CMBS, private REITs, and public REITs.

Asset types have proliferated as well. China's real estate resource base is rich, and because REITs began with infrastructure, assets like hydropower, wind, nuclear, and solar have all become relevant to real estate professionals. We shouldn't limit our thinking to buildings alone — data centers and 5G towers matter too.

The industry has also developed a full value chain running from Pre-REITs to Post-REITs management. Private equity funds incubate assets at the Pre-IPO stage, take them public, and then manage them in their listed form — drawing on the accumulated expertise of operators like Yuexiu and leading U.S. REITs managers in market cap management, risk control, and portfolio expansion through follow-on fundraising.

Looking ahead, I expect a far broader REITs ecosystem to take shape, spanning policy, investment, development, operations, services, and research — a lifecycle in which immature projects are nurtured through the collaboration of financial capital, developers, and operators, packaged into REITs, and exited in a clean, closed-loop structure. Not a sales cycle, but an asset cycle.

In closing, I want to offer a verdict very different from the "Iron Age" framing I raised earlier.

We are actually living in a Diamond Age — diamonds are simply rare, buried deep, and invisible to most. "Assets are king; operations are king" — that is the defining condition of the Diamond Age. What we face is a wholesale reshaping of business models. All the figures and histories that came before will pass; the wheel of history turns forward without pause.

The REITs ecosystem is one of the most important arenas to watch — and quite possibly the central protagonist in the reshaping of China's investment landscape. I won't pretend to offer specific investment tactics right now; the market is still in constant, living flux. But the REITs ecosystem — that I can see clearly. Asset value will be remade. The convergence of finance and real estate will accelerate and deepen. And specialized, precision-driven asset operations and management will become the defining competitive edge of this market.

That is my perspective on the reshaping of China's real estate investment landscape in 2025. Thank you.

more +

-

2025 APREA Asia Pacific Real Estate Leaders Summit Successfully Concluded in Singapore

2026-06-18

APREA Asia Pacific Real Estate Leaders Summit

The Asia Pacific Real Estate Leaders Summit is APREA's annual flagship event and the centerpiece of its 20th Anniversary celebrations.

Held under the theme "Building Future Assets Together," the Summit convened more than 205 global industry leaders for in-depth analysis of market trends, capital flows, and innovation across high-growth sectors. Attendees gained access to exclusive insights, direct dialogue with top-tier decision-makers, and a front-row view of the opportunities reshaping the industry.

Sigrid Zialcita, CEO of the Asia Pacific Real Estate Association (APREA), delivered the opening address.

John Lim, Chairman of APREA and Chairman of JL Family Office, delivered the welcome remarks.

Kelvin Tay, Managing Director and Chief Investment Officer for South Asia Pacific, UBS, delivered a keynote address.

Ronald Tan, Senior Vice President, Capital Markets, Singapore Exchange (SGX), delivered a keynote address.

David Chen (陈晓欧), Chairman of APREA China Chapter and Chairman & CEO of F.O.G Capital & Asset Management Group, delivered the closing remarks.

Panel 1: Commercial Real Estate — New Trends, New Directions, and What Lies Ahead

Panelists:

-

Pak Man Yuen, Managing Director, Blackstone

-

Josephine Yip, Managing Director, Real Estate Asia Pacific, La Caisse (formerly CDPQ)

-

Karol Piovarcsy, Board Member, ZDR Investments SG VCC

Moderator: Hank Hsu (许汉斌), Co-Founder & CEO, Forest Logistics Properties

Panel 2: Redefining Investment in High-Growth Sectors

Panelists:

-

Hardeep Sachdeva, Senior Partner, AZB & Partners

-

Andrew Lee, Director and Head of Investments, Singapore, Southeast Asia & Korea, BlackRock

-

Pushkar Kulkarni, Managing Director, Infrastructure & Sustainable Energy, CPP Investments

-

Kong Lingyi (孔令艺), Managing Director & Chief Investment Officer, SCGC Realty Capital

Moderator: Mitchell McCallum, Executive Director, MSCI

Panel 3: Japan — Bright Prospects in the Land of the Rising Sun

Panelists:

-

Masafumi Manno, President & CEO, Diamond Realty Management Inc. (DREAM)

-

Shai Greenberg, Senior Director, Japan Capital Markets & International Capital, Jones Lang LaSalle K.K.

-

Makoto Hideshima, Chief Investment Officer, KenedixAsia Pte. Ltd.

-

Harsh Narang, Managing Director, Rava Partners

Moderator: Jason Chan, Director, Fund Solutions, Vistra

Fireside Chat

Guest: Michael Smith, Chief Executive Officer, Hongkong Land

Moderator: Anita Kapoor, International Television Presenter

Panel 4: REIT Market Trends

Panelists:

-

An Chen, Senior Vice President and Portfolio Manager, AEW Capital Management

-

Hideki Yano, Managing Director, Consonant Investment Management Co., Ltd.

-

Kranti Mohan, Partner, Cyril Amarchand Mangaldas

-

Kok Siong Ng, Chief Financial Officer and Executive Director, Link Asset Management

-

Simon Garing, Chief Executive Officer and Executive Director, Stoneweg Europe Stapled Trust

Moderator: Adam Woodward, Head of M&A Tax and Australia Real Estate & Funds, Alvarez & Marsal

Panel 5: The Infrastructure Inflection Point

Panelists:

-

Hironobu Nakamura, CEO, Canadian Solar Asset Management K.K. (CSAM)

-

Meghana Pandit, Chief Financial Officer, IndiGrid

-

Deb Hajara, Senior Director, Ontario Teachers' Pension Plan

-

Matt Dimond, Managing Director, Client Capital, Sequoia Investment Management Co. Ltd.

Moderator: Jennifer Tay, Asia Pacific Infrastructure Leader, PricewaterhouseCoopers Singapore

Panel 6: Into the World of Family Offices

Panelists:

-

Terence Tang, Chief Executive Officer, Atelier Capital Partners

-

Norman Ho, Senior Partner, Corporate Real Estate, Rajah & Tann Singapore LLP

-

Andy Lim, Founder, The Land Managers

Moderator: Christine Li, Head of Research, Asia Pacific, Knight Frank

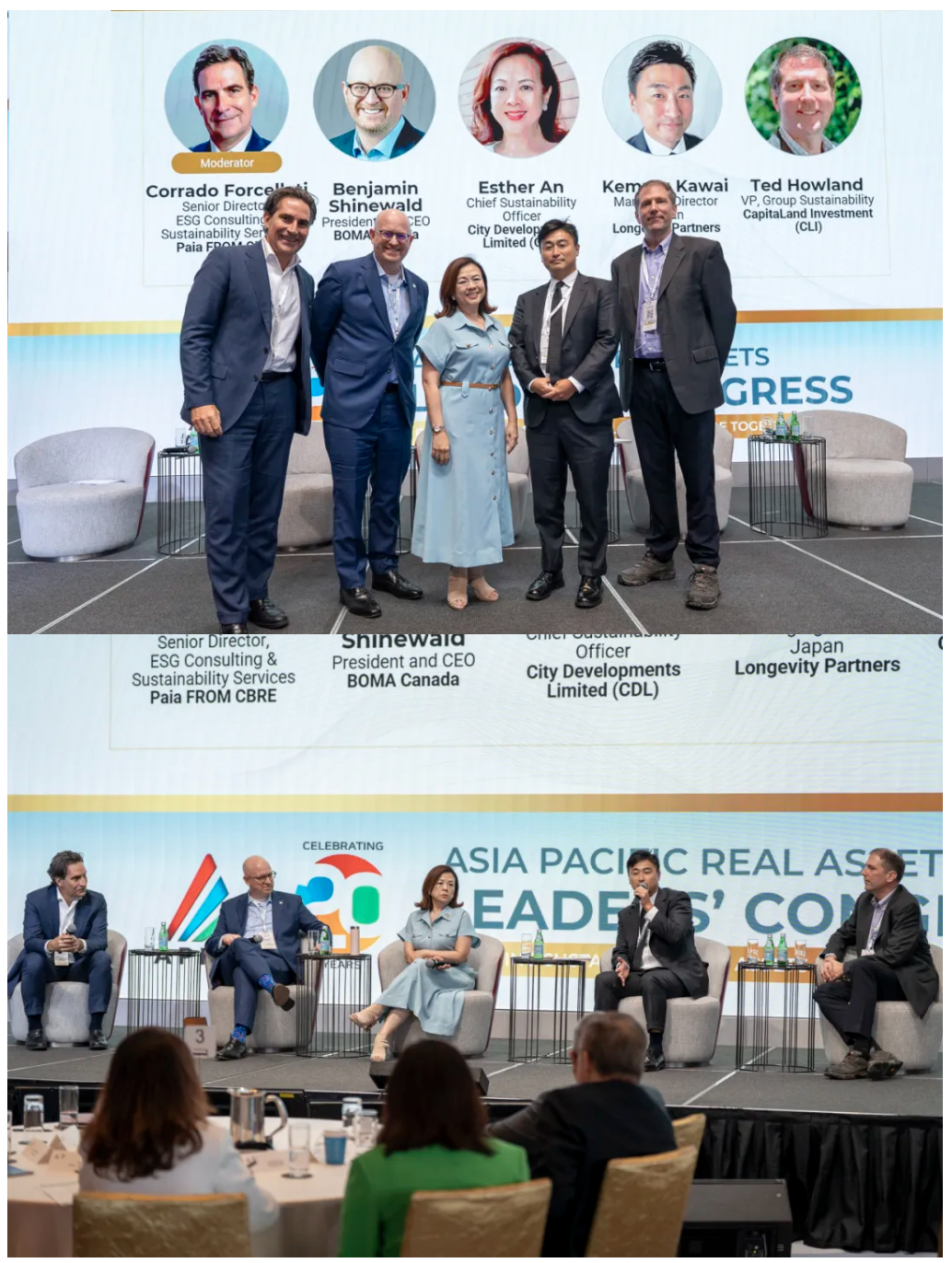

Panel 7: ESG — The Defining Issues of Our Time

Panelists:

-

Ted Howland, Group Vice President, Sustainability, CapitaLand Investment (CLI)

-

Esther An, Chief Sustainability Officer, City Developments Limited (CDL)

-

Kemmu Kawai, Managing Director, Japan, Longevity Partners

Moderator: Corrado Forcellati, Senior Director, ESG Advisory and Sustainability Services, CBRE

Panel 8: Asia Pacific Strategy for Global Investors

Panelists:

-

George Agethen, Managing Director, Real Estate Asia Pacific and Latin America, CDPQ

-

Ivy Ng, Chief Investment Officer, Asia Pacific, DWS

-

Han Hwee Chin, Managing Director, Global Investments and Portfolio Strategy, Real Estate, GIC

-

John Pattar, Partner and Head of Asia Real Estate, KKR

Moderator: Edwin Wong, Partner, Baker McKenzie

With Sincere Thanks to Our Sponsors

For their generous support of this Summit

Official Website: https://congress.aprea.asia

more +

-